Launching an all new card suite for SoFi

SOFI

MANUFACTURING

STRATEGY

PARTNER MANAGEMENT

SoFi's original card suite was built to serve everyone, which meant it served no one particularly well. I led the design and production of a new family of six cards, each mapped to a specific member persona and FICO range. The work connected physical design, manufacturing logistics, and commercial strategy into a comprehensive mature card business, all done in record time.

Coming soon

ROLE

Senior Manager

& Partner management

TEAM

Product manager, card ops,

three agencies

CROSS-FUNCTIONAL PARTNERS

CEO, Executive leadership, VP Brand, VP Marketing, VP Business, Card Ops

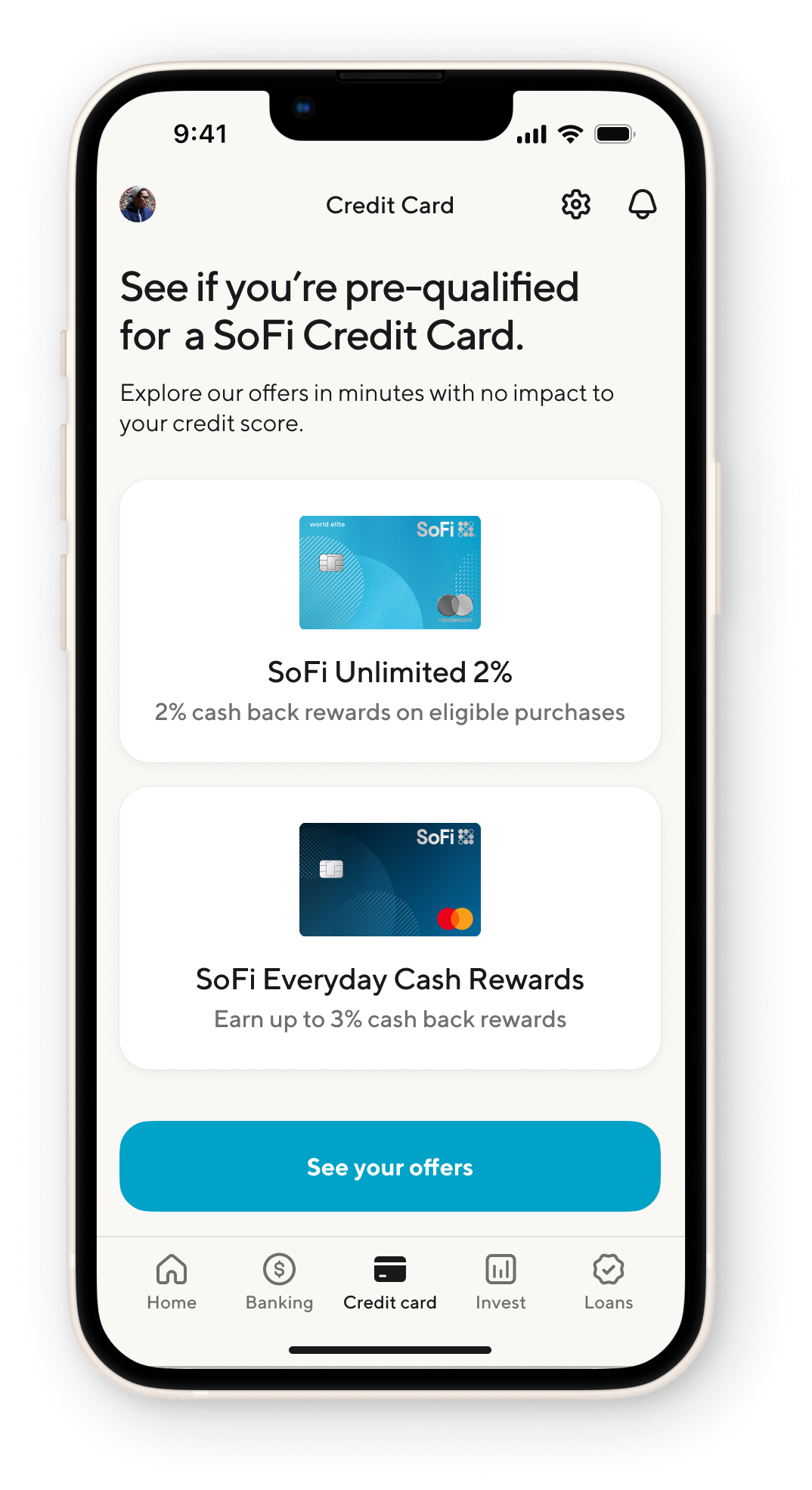

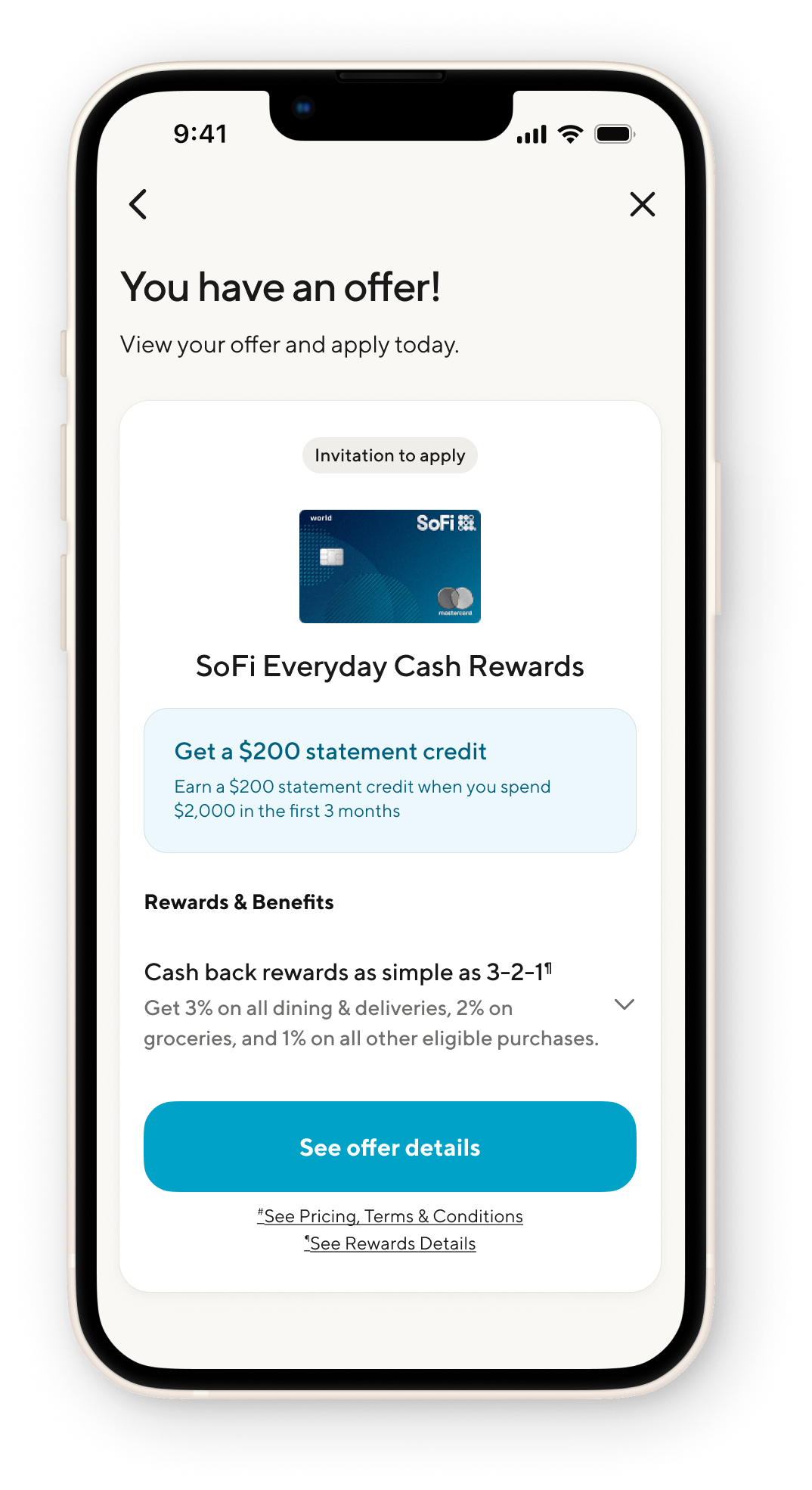

Business case for new cards

The original 2% card was designed to cast the widest possible net. In practice, that meant approving applicants across a broad FICO range, including segments that carried disproportionate risk and charge-off exposure. The card business was absorbing losses it didn't need to absorb.

The solution wasn't a better card. It was the right set of cards. By creating a tiered suite mapped to specific personas and credit profiles, we could tighten targeting, reduce risk exposure, and unlock retargeting opportunities that the single-card model couldn't support. New cardholders would be matched to the product built for them. Existing members would have a clear upgrade path.

That strategic unlock required something neither the design team nor the business had done before: designing, approving, and manufacturing multiple physical card products simultaneously, on a fixed timeline, with external vendors and Mastercard sign-off in the critical path.

Color & Research

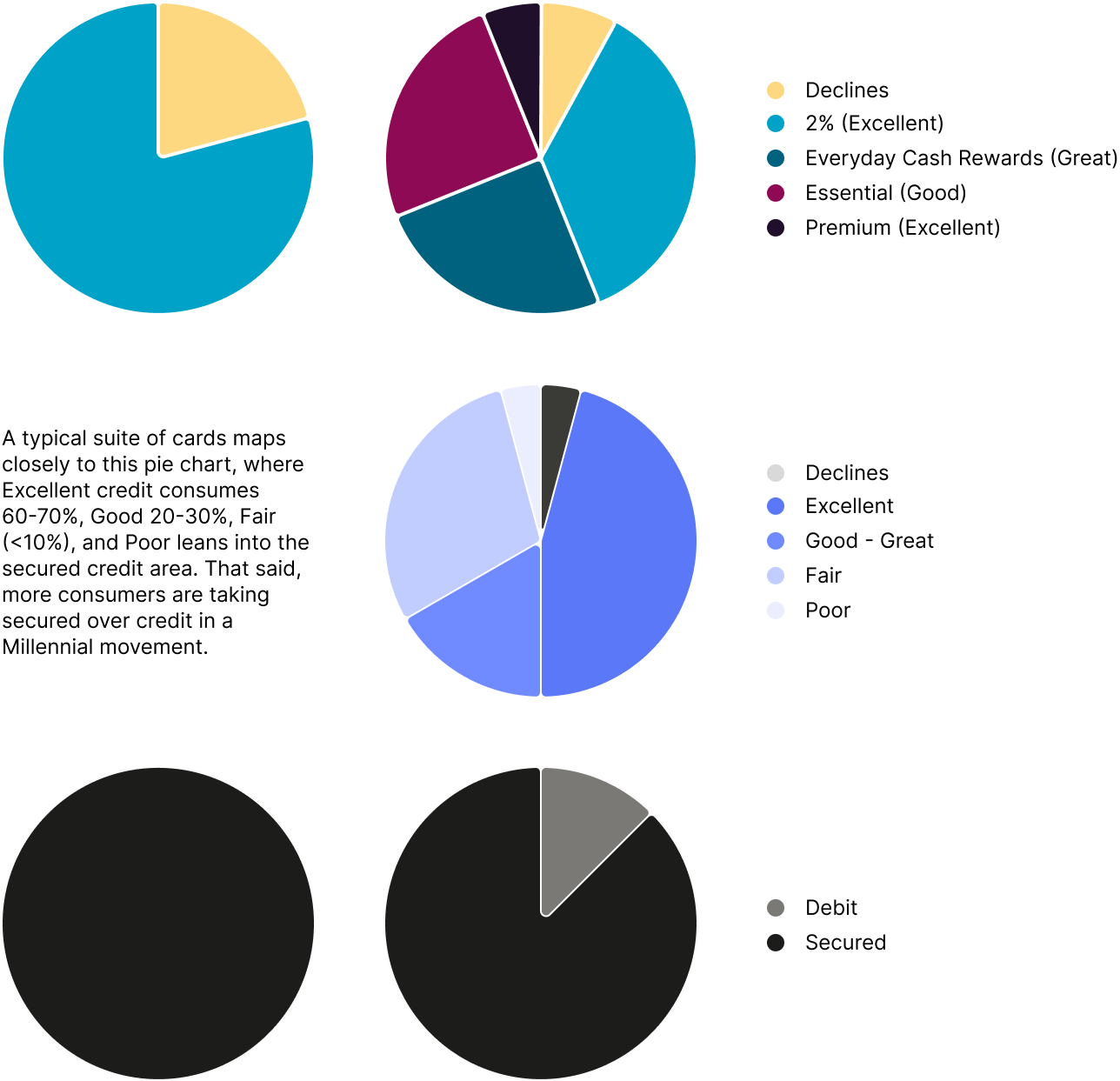

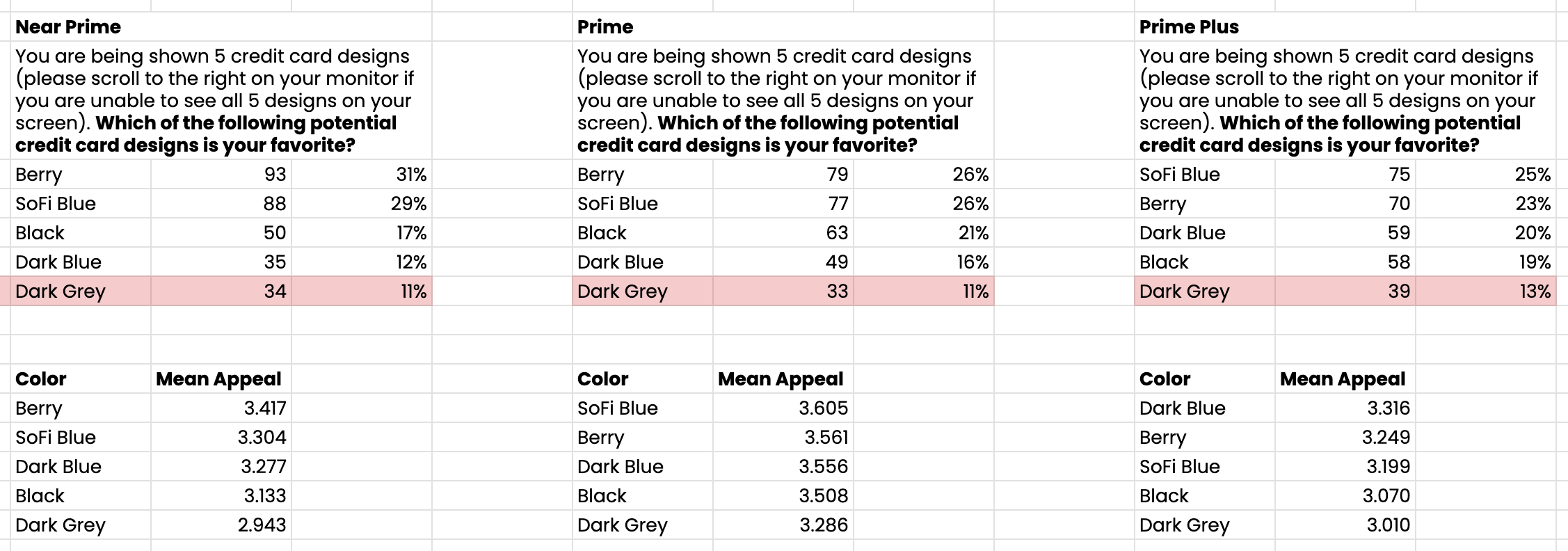

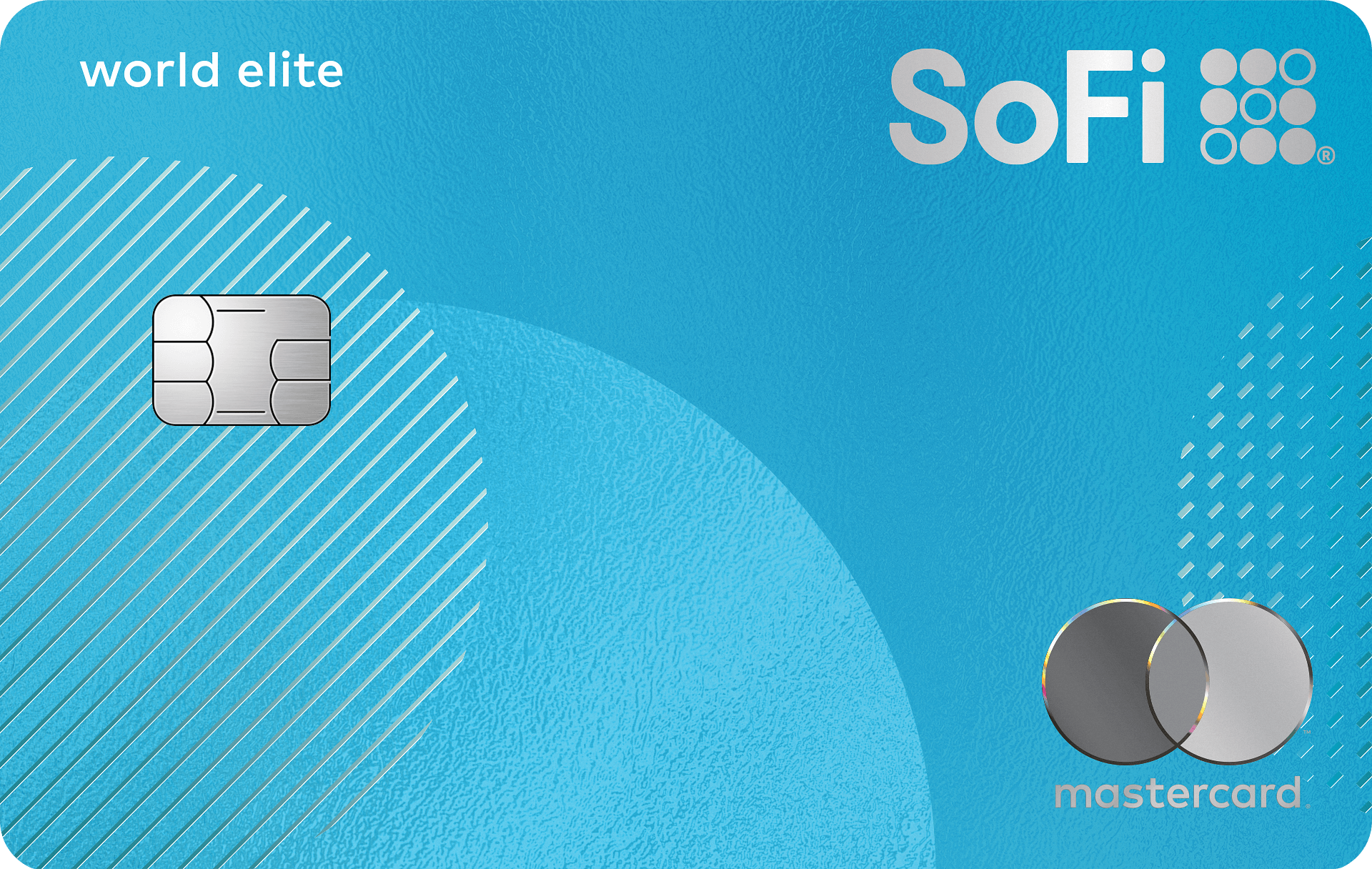

We ran a series of tests across colors, perks, benefits, and designs. With the expansion of our card suite, we had a color issue to address. The SoFi Blue card was our signature card, but it also wasn’t quite a premium card. In addition, we had two color palettes across brand and product.

Research and industry norms eliminated roughly 50% of our colors. I took the rest and established a range for the cards to blend across. We reserved black for our a future premium card.

With sample cards in hand, we asked potential members to match the card with the set of benefits they thought it best aligned to. In addition, we captured FICO range data to inform us which cohort preferred which card. As hypothesized, the younger early credit users preferred a more vibrant card. Although SoFi blue was the preferred choice of the prime range, and black was reserved, we chose dark blue for the second cohort.

Member experience

Touchpoints

It’s not only about how the card looks digitally, in your wallet, or feels in your hands. It’s about usage, whether you’re swiping, dipping, or tapping, we wanted to make sure the design was considered in every scenario.

Card construction

Layers

How our card is constructed plays a critical roll in how you design and print on it. For SoFi, a signature blue colored core was a branding element. That core sandwiches the antennae. You then print your designs on that core, where the base color has implications.

Back Perso

Colored Core

Antennae

Colored Core

Front Print

Printed layers

To create rich colors over a blue core, we needed to somewhat artificially create a white base. Without, colors would never be accurate. As you build the design, you print in plates to create the desired blending, layers, knockouts, and more.

Foil

SoFi Blue

10% White

Embossing

Details matter

Small details can have a big impact. We obsessed over the right colors, textures, and finishes to create a card that feels premium and reflects the SoFi brand.

Standard

Mastercard sticker

10% white litho over foil

Ink knockout

for foil passthrough & PLP embossing

Ink knockout to metal foil layer (appearance of metal)

Foil layer

SOFI BLUE

PMS: 234

CMYK: 17 100 6 18

RGB: 166 2 97

HEX: #A60261

How we ran it

Leading cross-vendor work at scale

This project was less about manufacturing informing design and more about design leading the manufacturing process. I took charge of coordinating a complex effort that involved three agencies, a card manufacturer, a distributor, and Mastercard's brand compliance team. Each of these parties had their own independent workflow, and their own internal contacts. I developed a unified process and set of documents to guide each card project.

Each timeline was fixed by business commitments. Working backwards from the launch date, I mapped every dependency: artwork approval windows, Mastercard review cycles, print plate production, embossing lead times, physical sample reviews, and distribution scheduling. Any delay at any stage compressed the next one, which provided a clear signal of where to apply pressure, descope, or find opportunities to accelerate. The only way to hold the date was to anticipate the compression before it happened and escalate early.

We held the timeline. In some cases we were ready before launch. We didn’t exceed our very small budget. And I gave every team downstream, card ops, marketing, product, the blueprint they could use to run this process again without starting from scratch. Improved shared knowledge enhanced our accountability, which consequently led to increased speed.

Outcomes

What shipped and what it enabled

Six cards launched on schedule. The new suite introduced distinct personas with aligned FICO ranges, bringing SoFi's targeting in line with industry standards and reducing charge-off risk. Account opens increased and redistributed across the portfolio in a healthier pattern.

Member response exceeded internal expectations. There was early skepticism about the purple card internally. Once members had it in hand, it became a standout. The ECR card was received as the clearest value proposition in the portfolio — benefits that matched or exceeded what members expected going in.

Commercially, the new card suite unlocked retargeting capabilities that didn't exist before. Acquisition could now be matched to product, not just to brand. We could better target our members with a card that best fit their needs, and matched with our credit card financial best practices. That's the structural change the business needed, and the card designs were the thing that made it real. Now, we can operate with more intentional marketing, and more intelligent personalized recommendations.

Prime Plus (720+)

Not

targeted

Prime (660-719)

Near Prime (580-619)

With one card for everyone, we missed 40% of the market and had lower application approvals.

Pre-screen offers

Appendix

The sprint was time-boxed by design. It was two intensive days between design, marketing, and our business partners. Design ran our own sessions with multiple daily check-ins for rapid paced feedback loops.

The goal was to deliver a broad spectrum of possibilities, eliminate the wrong directions fast enough that the right ones with concrete alignment had the space to emerge. We ruled out three concept families before arriving at the system that shipped. What you see below is a wide variety of the fast failures, a necessary and under appreciated step to get to the best outcome.

Let’s get to work

I'm always interested in connecting with fellow leaders, exploring new opportunities, and discussing, well, just about anything.

Get in touch

Michael Spiegel

© 2026 Two Pixels, LLC. All rights reserved.

Home

Work

About

Substack

Home

Work

About

Blog

Get in touch